Sanjoy Sen is a chemical engineer. He contested Alyn and Deeside in the 2019 general election.

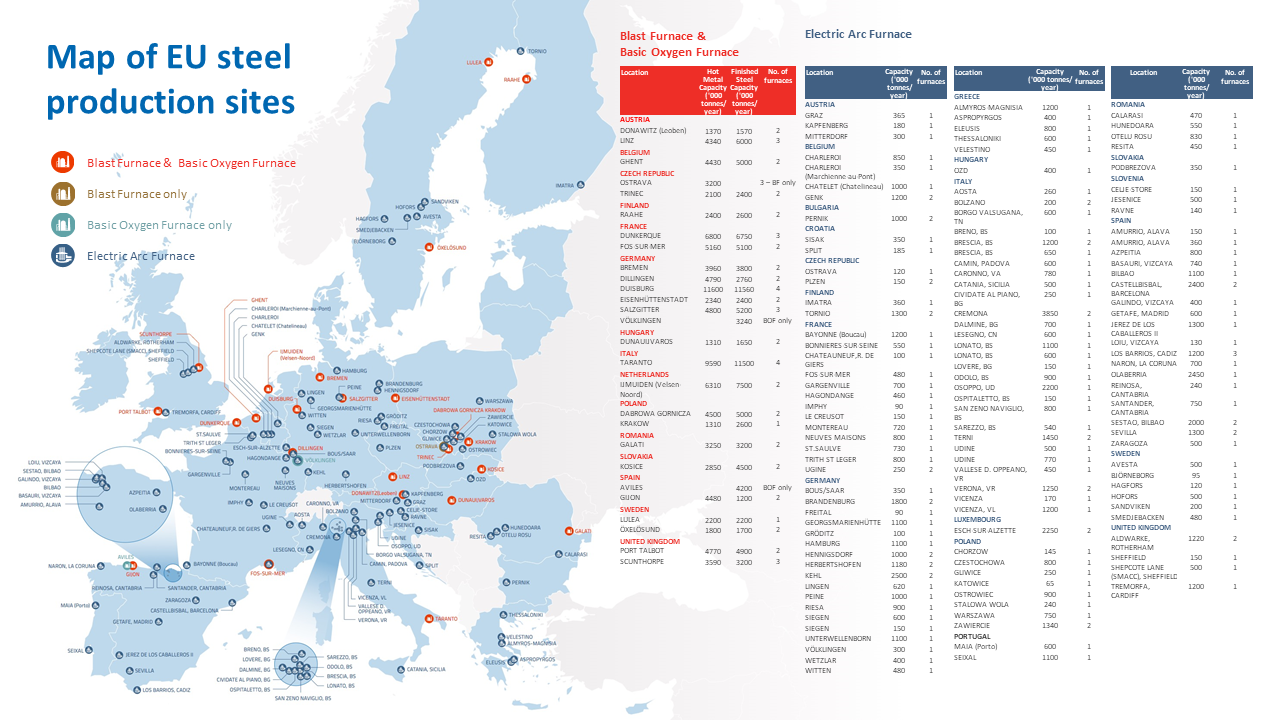

Labour has just intervened to keep the British Steel Scunthorpe works going with further measures (including nationalisation) still on the table. Whilst Britain’s last blast furnaces remain lit for now, major challenges remain. Globally, steel companies face a daunting combination of falling demand, Chinese competition and ever-rising costs.

Questions abound: how did we get here, what next for steel and what are the political implications?

Decades of decline

Little did I know it but my stint at Scunthorpe was to coincide with British Steel’s peak. Painful re-structuring had seen major sites close: Corby (1979), Consett (1980), Shotton (1980), Ravenscraig (1992). But a competitive global player emerged and by the early nineties, it was the world’s fourth-largest producer.

Soon afterwards, global supply began to ramp up (especially from China) and established competitors merged. British Steel and the Dutch giant Hoogovens formed Corus in 1999 and were later swallowed up by India’s Tata in 2007.

The following year, however, the global economic crisis hit steel-hungry sectors hard, especially construction. That knocked 35 million tonnes (almost 20 per cent) off European demand and it hasn’t returned. Facing mounting losses, Tata sold off Redcar in 2011 but its new owners, Thailand’s SSI, threw in the towel just four years later.

With losses running at a million pounds a day, Port Talbot might have gone the same way. Instead, following a £500 million injection from the Sunak administration, Tata will replace its blast furnaces fed by virgin materials (iron ore, coke) with an electric arc furnace (EAF) fed by scrap metal. But with a phased transition rejected, thousands of jobs at the vast Margam works have already been lost.

Tata offloaded Scunthorpe to Greybull Capital in 2016 who resurrected the British Steel brand. It lasted barely three years before entering liquidation with current owners, China’s Jingye, stepping in in 2020. Again, with mounting losses (£700,000 a day), the proposed solution was a state-backed EAF transition.

But whilst Jingye initially sought £600 million, they later upped their demands – and with the Chinese reportedly curtailing blast furnace raw material orders, Starmer was forced to act.

What next?

Steel remains an economic cornerstone, essential for key sectors such as automotive, machinery and construction. But it’s long been challenging to make the stuff profitably.

Back in my day, no Chinese manufacturer was even in the global top 20; by 2021, its annual output exceeded a billion tonnes, more than the rest of the world combined.

Today, China faces major challenges of its own, with falling domestic demand and Trumpian tariffs. With that likely to push Chinese exports elsewhere, the UK (and others) will continue to rely on quotas and tariffs to stem the tide.

Running costs are now also soaring. For virgin (blast furnace) steelmaking, iron ore prices have trebled over the past decade, and as EAF’s share of world’s steel output approaches 50 per cent, global scrap supply looks set to tighten. Worse still for British EAF operators are our sky-high electricity prices – far higher than our competitors.

Also hanging over the industry is the £4.4tn required to tackle sector emissions. Right now, the Swedes are early leaders with HyBRIT, a new direct-reduced iron (DRI) process using hydrogen from renewables. State aid has been dished out pretty generously across the EU (especially in Germany) to support the transition to green steel.

Meanwhile in France, ArcelorMittal will phase out its Dunkirk and Fos blast furnaces by 2030 with a combination of EAFs and DRI, supported by €850m of government funding.

Political implications

Governments are confronted by tough choices between unpalatable options. These range from allowing market forces to wipe out domestic steelmakers through to bearing the losses of nationalisation. We are not alone in wrestling with such challenges: Nippon Steel’s takeover of loss-making US Steel was blocked by the Biden administration, citing national security issues; the Trump position is constantly shifting.

Post-Redcar, the UK has opted to keep foreign owners afloat. The retention of a domestic steel industry is now seen as vital on both sides of the House, with Covid-19 and global instability exposing the vulnerability of global supply chains. And whilst EAF technology is improving, losing Scunthorpe’s blast furnaces would leave the UK rare amongst developed nations in being unable to produce its own higher-quality virgin steels.

Right now, saving Scunthorpe (for now, at least) might provide a welcome blip for Sir Keir Starmer after a difficult first year in office. Even local Conservative MPs and Reform back nationalisation as an option.

But all isn’t plain sailing: Plaid Cymru are enraged that Port Talbot wasn’t saved, and the SNP want similar support for the Grangemouth oil refinery.

With protecting British jobs and ensuring national security of supply both high up the agenda right now, further demands could follow. These might include local content requirements for infrastructure projects or a re-think on North Sea oil and gas licensing.

If we are going to back our domestic steel industry, there are a couple of levers available to government. Firstly, British blast furnaces rely on imported raw materials: that could be addressed by the Cumbrian coal mine, which had the rug pulled from under it by Angela Rayner, and was intended to supply metallurgical users.

Secondly, those power prices need tackling. UK industrial electricity costs are roughly double and quadruple those in Germany and the USA respectively. Sticking to the commitment to decarbonise the grid by 2030 could keep things that way for the foreseeable future. As I said, tough decisions await.

![NYC Tourist Helicopter Falls into Hudson River, Siemens Executive and Family Among Those Killed [WATCH]](https://www.right2024.com/wp-content/uploads/2025/04/NYC-Tourist-Helicopter-Falls-into-Hudson-River-Siemens-Executive-and-350x250.jpg)

![Red Sox Fan Makes the ‘Catch of the Day’ with Unconventional ‘Glove’ [WATCH]](https://www.right2024.com/wp-content/uploads/2025/04/Red-Sox-Fan-Makes-the-‘Catch-of-the-Day-with-350x250.jpg)

![Green Day’s Cringe Trump Diss Ends in Fire and Evacuation [WATCH]](https://www.right2024.com/wp-content/uploads/2025/04/Green-Days-Cringe-Trump-Diss-Ends-in-Fire-and-Evacuation-350x250.jpg)

![Bikini Clad Spring Breakers Prove Our Education System is Failing Students [WATCH]](https://www.right2024.com/wp-content/uploads/2025/03/Bikini-Clad-Spring-Breakers-Prove-Our-Education-System-is-Failing-350x250.jpg)

{kind=link}